The roller coaster ride of total returns on the S&P 500! (Updated to October 2025)

- November 17, 2025

The roller coaster ride of total returns on the S&P 500! 🎢📈 (Updated to October 2025)

Imagine investing $10,000 in the S&P 500 (with dividends reinvested and adjusted for inflation). How much would you have today depending on when you started?

Last 5 years: +73.84% → $17,384 (actual annualized return: 11.11%)

Last 10 years: +203.65% → $30,365 (11.16% annualized)

Last 15 years: +449.02% → $54,902 (11.41% annualized) ← the best horizon right now!

Last 20 years: +432.45% → $53,245 (8.39% annualized)

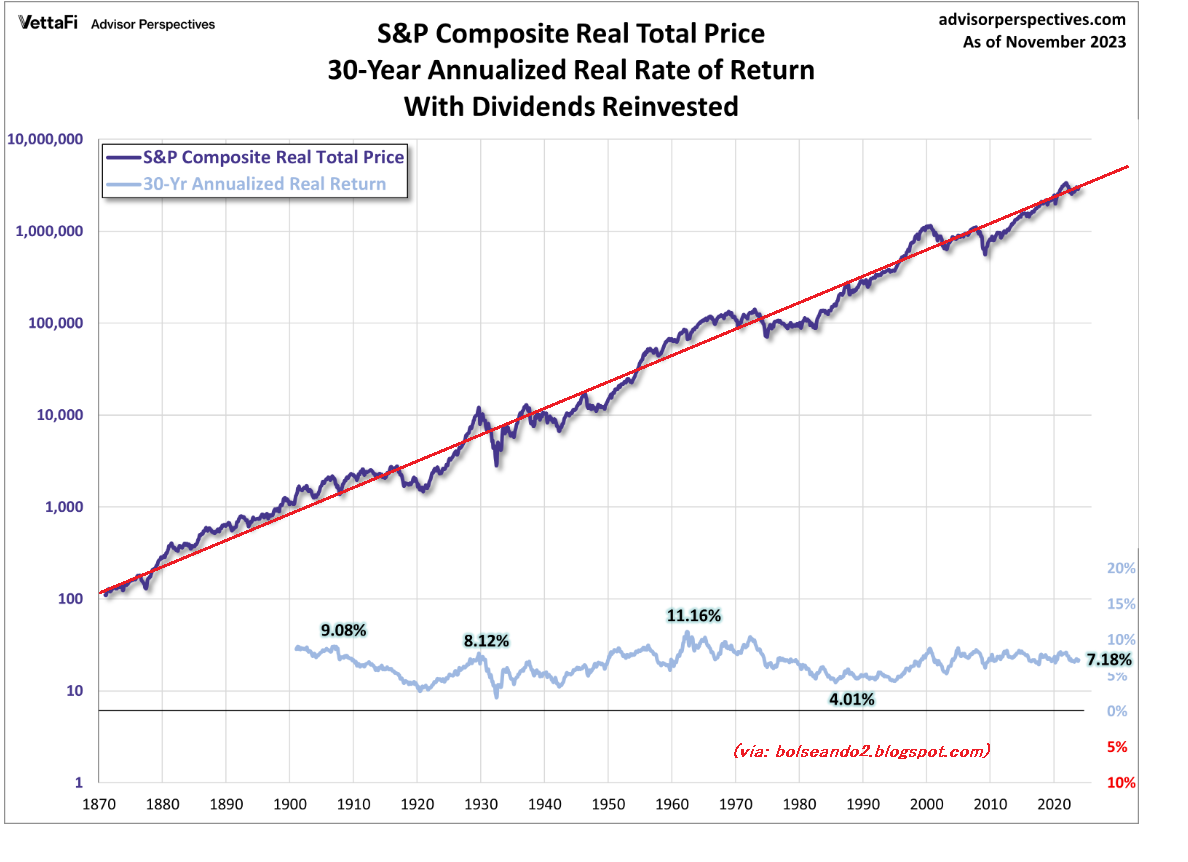

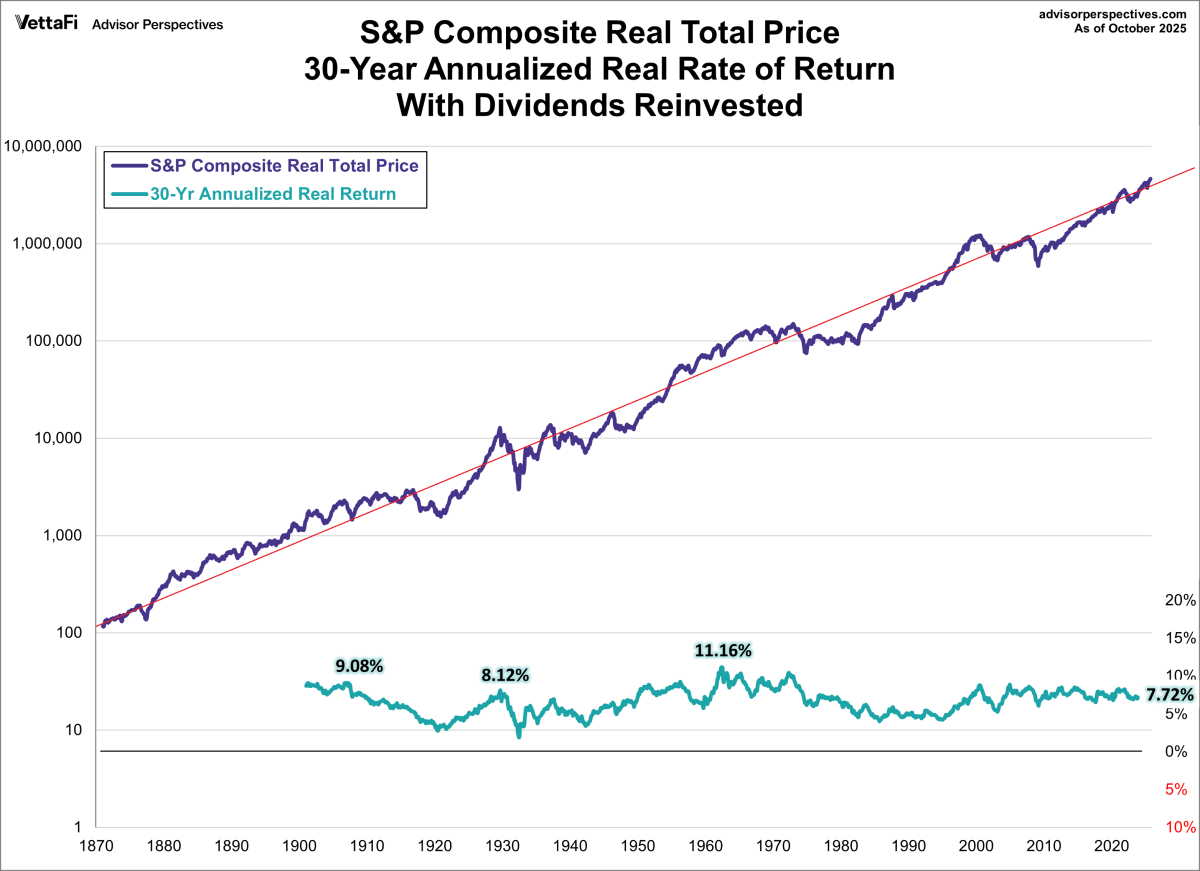

Last 30 years: +906.19% → $100,619 (7.72% annualized)

The longer the term, the less crazy the ups and downs are… but beware: if we had asked this same question in March 2009 (the bottom of the financial crisis), those same 5 years would have left you with only $6,654 in real purchasing power (-8.12% annualized). You would lose a third of the real value!